Winterkill losses

Alfalfa winterkill losses were significant in South Dakota, Minnesota and Wisconsin, with northeastern and central Wisconsin the hardest hit, according to Dan Undersander, forage agronomist with the University of Wisconsin – Madison.

Areas with heaviest losses and acreage impacted by winterkill were in southern South Dakota (just west of Interstate Highway 29) – 20,000 to 30,000 acres; central Minnesota – 20,000 to 30,000 acres; and northeastern and southwestern Wisconsin (70,000 to 100,000 acres).

Fields most affected were older fields and/or those where a late fall cutting was taken, Undersander said. Adequate snow cover likely provided winterkill protection east of Wisconsin, he added.

Excessive moisture levels were also causing grower challenges elsewhere. Rachel Freeman Long, field crop and pest management farm adviser with the University of California, said common leaf spot was common in alfalfa fields early this spring.

Thanks to a milder winter, alfalfa weevil larvae emerged early across the country’s midsection, according to extension entomologists.

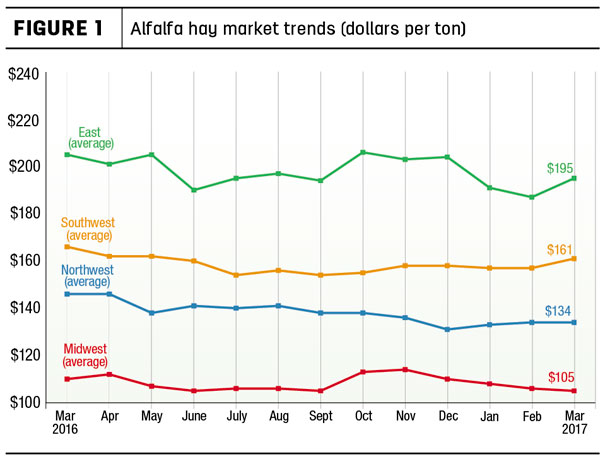

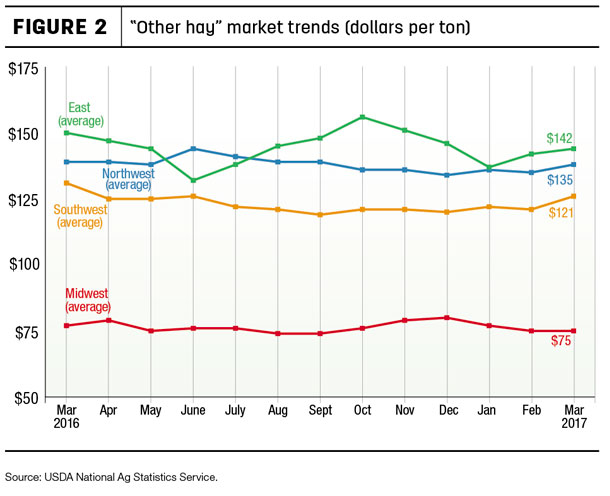

Alfalfa hay prices

The news was better for hay marketers. The latest available USDA monthly ag prices report was released April 27, summarizing March 2017 prices.

Alfalfa

The March 2017 U.S. average price paid to alfalfa hay producers at the farm level was $135 per ton, a $6 jump from February and the highest average since October 2016.

On a regional basis, March prices were higher in the East and Southwest (Figure 1). Within regions, the average price was up $19 per ton in New York, $15 per ton in Ohio and $10 per ton higher in California, Kansas and Missouri.

Compared to a year earlier, price changes were diverse: up $25 per ton in Nevada and $20 per ton in Montana, but $20 to $40 lower in seven states, led by Colorado, Idaho, New York, Texas, Utah and Washington.

Other hay

The March 2017 U.S. average price for other hay was estimated at $127 per ton, up $5 from February and $1 more than March 2016. Regionally, prices for other hay were up in the Southwest (Figure 2). Within regions, average prices for other hay were up $10 to $15 per ton in Nevada, Ohio, Oklahoma and Oregon.

Compared to a year earlier, price changes for other hay were also diverse: up $30 per ton in New York and $20 in Montana, but $15 to $29 lower in Iowa, Ohio, Oregon, Pennsylvania and Utah.

In the organic hay market, small square bales of Fair-quality alfalfa sourced from Oregon averaged $180 per ton, as did small square bales of Supreme alfalfa/grass hay sourced from Iowa. The USDA report summarizes organic hay sales held between April 13-26.

Alfalfa hay exports a record

While domestic hay markets mostly remained in the doldrums, hay exports picked up.

Aided by sales to China, U.S. alfalfa hay exports hit 271,174 metric tons (MT) in March 2017, likely the highest monthly total ever. Alfalfa hay sales to China were estimated at 121,730 MT. The next four markets (Japan, Saudi Arabia, United Arab Emirates and South Korea) combined to purchase 138,800 MT. The alfalfa hay exports were valued at about $77.75 million.

March 2017 sales of other hay totaled just over 144,560 MT, with Japan and South Korea combining to purchase about 121,350 million MT. March sales represented the highest total since April 2015. The other hay exports were valued at about $42.5 million.

March exports of alfalfa cubes and meal were the highest in several months.

Auction and market summaries

Here’s a peek at early May auction market summaries:

-

Southeast: Alabama hay prices were steady, with moderate supply and demand.

-

Southwest: All classes of California hay traded steady, with moderate demand. As of early May, first cutting was completed in southern and southwestern New Mexico, and 50 to 70 percent done in the Southeast. Alfalfa hay prices were steady, with trade and demand moderate. In Oklahoma, hay movement was at a near standstill as rain continued and fieldwork was put on hold.

Some first cutting will be too mature for dairy or horse hay buyers. Demand was moderate for dairy alfalfa and light to moderate for other offerings. Alfalfa yields are expected to be average to above average in much of central and western Oklahoma.

In Texas, most hay classes remained steady except for high-quality, new-crop alfalfa, which sold $15 higher on light to moderate movement. Utah hay prices were mostly steady to weak, with trading slow.

-

Northern Plains: In South Dakota, alfalfa and grass hay sold higher. Bedding in good condition sold higher; poor-quality bedding sold lower. In the Wyoming, western Nebraska and western South Dakota market, prices were mostly steady with activity and demand light in all classes.

-

Central Plains: In Nebraska, alfalfa and grass hay sold unevenly steady. Some cattlemen are buying up last year’s alfalfa supplies and stockpiling it for future use; while others are buying on a hand-to-mouth basis.

Colorado prices were steady with activity light and good demand in all classes. Producers state that demand is still strong, but most producers are sold out until cutting their new crop.

Southwest/south-central Kansas hay market activity was moderate to slow, with light to moderate demand for all classes of hay; prices were steady.

-

Northwest: In Idaho, alfalfa prices were steady to firm, with good demand. In Oregon, prices trended generally steady in a limited test, with heaviest demand for retail/stable hay. In the Washington-Oregon Columbia Basin, export and domestic alfalfa prices were steady to firm in a light test. Most interests were sold out waiting for new crop. New crop harvest was noted in the southern basin.

- Midwest: In Iowa, many producers are sold out and hoping to start first cutting in the middle of May. In Missouri, excessive moisture and flooding were the main concerns. Hay harvest thoughts were mostly put on the back burner as focus turned more to assuring survival of livestock.

The supply of hay is moderate, demand is light and prices are steady to weak. It remains largely a buyer’s market in Wisconsin, with overall prices steady and reduced prices on lower-quality hay.

- Northeast: In Pennsylvania’s Lancaster area, alfalfa varieties sold mostly steady. Large bales of grass hay sold $10 to $20 lower, while small bales remained mostly steady. Large bales of straw sold steady to weak while small bales sold firm on a light test.

Drought areas disappearing

At the end of April, about 90 percent of cropland acreage topsoil and subsoil moisture was rated adequate to surplus, based on USDA’s weekly Crop Progress report. The wet conditions sharply limited the numbers of days suitable for fieldwork in many states.

USDA’s World Agricultural Outlook Board said just 4 percent of U.S. hay acreage was located in areas experiencing drought as of May 2, down nearly 10 percent from a month earlier. Drought areas were primarily concentrated in Georgia and Florida, and in extreme southern California and Arizona.

Check out the hay areas under drought conditions (U.S. Drought Monitor).

Fuel prices lower

Fuel prices moved lower to end April, according to the U.S. Energy Information Administration (EIA). As of May 1, U.S. on-highway diesel fuel prices averaged about $2.58 per gallon, down 1.2 cents per gallon from a week earlier, but up about 32 cents per gallon compared to a year ago.

EIA estimated U.S. retail prices for regular gasoline averaged about $2.41 per gallon as of May 1, down 3.8 cents from the week before, but about 17 cents per gallon higher than a year ago.

Figures and charts

The prices and information in Figure 1 (alfalfa hay market trends) and Figure 2 (“other hay” market trends) are provided by NASS and reflect general price trends and movements. Hay quality, however, was not provided in the NASS reports. For purposes of this report, states that provided data to NASS were divided into the following regions:

• Southwest – Arizona, California, Nevada, New Mexico, Oklahoma, Texas

• East – Kentucky, New York, Ohio, Pennsylvania

• Northwest – Colorado, Idaho, Montana, Oregon, Utah, Washington, Wyoming

• Midwest – Illinois, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, South Dakota, Wisconsin

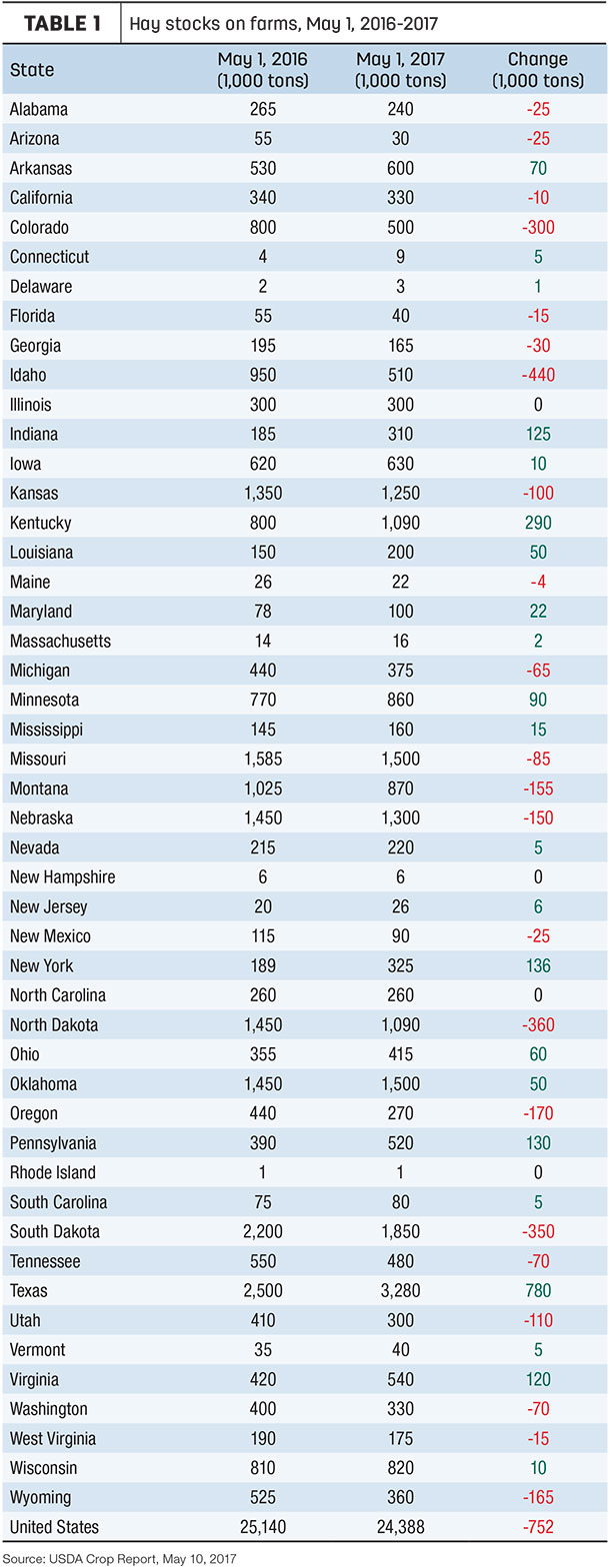

A summary

Hay stocks on farms: All hay stored on U.S. farms as of May 1, 2017, totaled 24.4 million tons, down 3 percent from the previous May. Disappearance from December 1, 2016 – May 1, 2017, totaled 71.4 million tons, compared with 69.9 million tons for the same period a year earlier.

With the exception of Nevada, hay stocks in most Western states are estimated lower than in 2016. The majority of the Eastern states reported higher stocks compared to the previous year due to a mild winter with no need to extend supplemental feeding. ![]()

-

Dave Natzke

- Editor

- Progressive Dairyman

- Email Dave Natzke