With spring in the air, the USDA releases the first 2017 crop acreage estimates on March 31.

Alfalfa

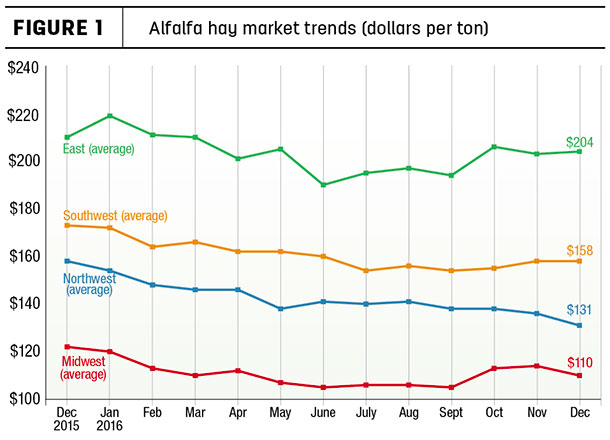

The December 2016 U.S. average price paid to alfalfa hay producers at the farm level was $129 per ton, down $1 from November and $20 less than a year earlier. U.S. average prices continue at a six-year low.

Other than Midwest states, where average prices were all lower, December prices in other regions were mixed. In the East, prices were up in New York and Pennsylvania but down in Ohio and Kentucky (Figure 1).

In the Northwest, averages were higher in Colorado but lower in Montana, Idaho, Utah, Oregon and Washington. In the Southwest, average prices were up in Arizona, New Mexico, Oklahoma and Texas but down in California and Nevada.

New York surpassed Kentucky as the price leader in December at $221 per ton.

Lowest average prices were in Nebraska ($79 per ton) and North Dakota ($80 per ton).

Other hay

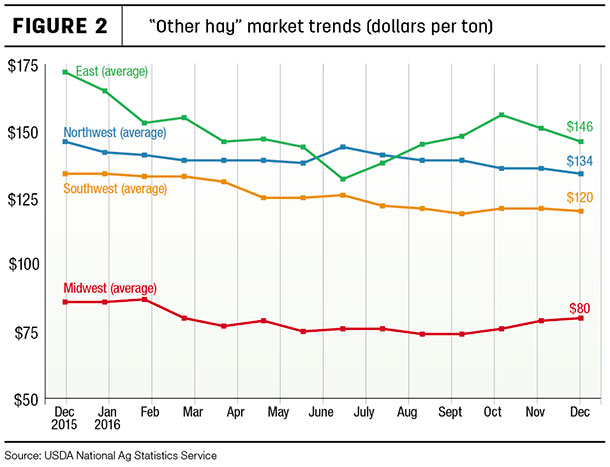

The December U.S. average price for other hay was estimated at $120 per ton, down $3 from November and $4 less than December 2015. With an exception of a small bump higher in the Midwest, averages were down in other regions.

Among individual states, producers in Pennsylvania saw a $15 per ton decline compared with a month earlier, while Nevada, Ohio, Oregon, and Washington posted declines of $10 per ton. Kansas saw a $11 increase.

Highest December 2016 prices were in New York ($189 per ton) and Pennsylvania ($173 per ton); lowest prices were in Minnesota ($59 per ton), Wisconsin ($67 per ton) and Nebraska ($68 per ton) (Figure 2).

Organic hay

With limited sales reports, large square bales of California-sourced premium- and supreme-quality alfalfa hay sold in a range of $228 to $375 per ton (delivered) for the period of Jan. 5 to Feb. 1, according to the USDA’s biweekly organic feedstuffs reports. Fair/good-quality alfalfa in large square bales sold in a range of $260 to $268 per ton.

Auction and market summaries

Like the groundhog, some hay buyer interest began to come out of hibernation in early February. Here’s a peek at auction market summaries:

- Southeast: Alabama hay prices steady; moderate supply and good demand.

- South Central and Southwest: In Oklahoma, demand for dairy alfalfa was moderate, while demand for dry cow and bunk hay was fairly good. Texas prices were mostly steady. Plenty of hay was available, but mileage/freight costs were a factor.

In California, all classes traded steady with moderate demand. New hay harvest was slowed by wet weather and cooler temperatures.

- Northern Plains: In South Dakota, all classes of hay remained steady on moderate demand. Winter storms made transportation difficult and boosted demand for bedding material. Montana alfalfa hay sold steady to $10 higher as buyers entered the market.

With the start of calving season, straw demand was very good. In Wyoming and western Nebraska, prices were steady with activity light and demand moderate. Producers reported hay moving in from the east.

- Central Plains: In Nebraska, alfalfa and grass hay, dehydrated alfalfa pellets and ground and delivered hay sold steady. Demand was starting to pick up for alfalfa and grass hay. In Kansas, the hay trade picked up slightly for ground and delivered alfalfa.

Demand remained moderate for all other classes of hay; prices remained steady. Colorado prices were mostly steady with activity light. Producers reported an increase in interest and demand.

- Northwest: In Idaho, feeder alfalfa trade remained slow with light to moderate demand, but there’s more interest on the buyer side.

In Washington and Oregon’s Columbia Basin, export and domestic alfalfa was firm in a light test. Trade remains slow. In Oregon, hay prices trended generally steady in a limited test. Most demand was for retail/stable hay.

- Midwest: In Illinois, hay trade was active with moderate to poor demand on large offerings. In Iowa, supply was adequate while demand was slow; prices remained steady. Wisconsin hay prices were steady with little demand; lower-quality hay was discounted with large supplies.

Some markets mentioned better demand for bedding materials. In Missouri, supplemental feeding moved into full swing as stockpiled pastures diminished.

- Northeast: In Pennsylvania, alfalfa hay sold steady on limited comparable receipts; mixed hay sold mostly steady to $10 higher; grass hay sold unevenly steady on a heavy supply. In the Lancaster area, alfalfa varieties sold mostly steady to $10 higher; grass hay sold mostly steady to $10 lower.

Fuel price outlook

Due to the importance of fuel in hay production input costs, Progressive Forage is beginning a regular look at fuel prices. Cassidy Woolsey contributed to this month’s report, summarizing a Washington Hay Conference presentation by Tina Hampton, R.E. Powell Distributing.

As of Feb. 1, the U.S. Energy Information Administration (EIA) estimated the U.S. on-highway diesel fuel prices averaged $2.56 per gallon, down about 2 cents per gallon from two weeks earlier, but up about 53 cents per gallon compared to a year ago.

West Coast prices averaged about $2.84 per gallon, up 57 cents from a year earlier. Although Western diesel fuel prices could decline slightly, Hampton doesn’t expect them to fall to last year’s levels. She estimated Western diesel prices will average about $2.80 per gallon in 2017, up from last year’s average of $2.40 per gallon.

The scenario is somewhat similar for gasoline. As of Feb. 1, EIA estimated U.S. retail prices for regular gasoline averaged nearly $2.30 per gallon, also trending about 50 cents per gallon higher than a year ago. The West Coast was higher at $2.68 per gallon.

Dairy outlook: Big ‘Mo’ continues to grow

U.S. milk production momentum pushed through the final month of 2016, gaining strength from more cows and greater milk output per cow.

Momentum is built on mass and velocity, and December continued a four-month roll in which U.S. milk production increased at least 2 percent from the same month a year earlier.

December 2016 U.S. cow numbers were up 38,000 head compared to a year earlier, and up 53,000 head in the major states. Thanks to genetics, feed and management, milk production per cow in the 23 major states was the highest December total since the USDA started tracking those numbers in 2003.

Looking ahead to 2017, cow numbers are expected to grow throughout the year, with annual milk production projected at 217.1 billion pounds. If realized, production would be up about 2.2 percent from 2016’s estimate.

Despite the higher production, the USDA forecasts the average U.S. all-milk price to be in a range of $17.60-$18.40 per hundredweight, up about $1.75 per hundredweight from 2016.

Beef cattle outlook: Price headwinds

After declining for most of 2016, fed cattle prices saw a slight resurgence in late December. However, fed steer price increases are expected to experience headwinds during the first half of 2017, primarily due to the abundant supply of cattle on feed and expected higher year-over-year marketings during the first half of the year.

Like fed cattle prices, cutter-cow prices are expected to remain under pressure well into 2017 due to the expected increase in the supply of animals available to be marketed.

Figures and charts

The prices and information in Figure 1 (alfalfa hay market trends) and Figure 2 (“other hay” market trends) are provided by NASS and reflect general price trends and movements. Hay quality, however, was not provided in the NASS reports.

For purposes of this report, states that provided data to NASS were divided into the following regions:

- Southwest – Arizona, California, Nevada, New Mexico, Oklahoma, Texas

- East – Kentucky, New York, Ohio, Pennsylvania

- Northwest – Colorado, Idaho, Montana, Oregon, Utah, Washington, Wyoming

- Midwest – Illinois, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, South Dakota, Wisconsin