Impacted by tariffs, September shipments to China totaled 53,032 MT, the smallest volume since January 2016. On an annual basis, China has been the leading U.S. alfalfa hay market since 2014, but maintaining markets there is not getting any easier, said Christy Mastin with Eckenberg Farms Inc., Mattawa, Washington.

A somewhat stronger Chinese dairy industry has boosted hay demand, but the window of opportunity is small. Any shipments must depart the U.S. in December to reach destinations before the Chinese New Year, Feb. 5, 2019. There are also fears that escalating trade war rhetoric could result in additional tariffs, cancelled orders and demands for price reductions.

Competitors for the Chinese hay market have their own challenges, Mastin said. Canada and Spain do not have adequate alfalfa quantities to supply all of that market, and the drought in Australia has diminished oaten and wheat hay supplies for export.

On the flip side, Saudi Arabia continues its phaseout of water use for domestic forage production, a program initiated in 2016. To fulfill its growing forage needs, Saudi Arabia has been aggressive in buying hay and hay-producing land in the southwest U.S. As a result, Saudi Arabia imported a record 62,341 MT of U.S. alfalfa hay in September, surpassing China as the leading market for U.S. alfalfa for the first time ever.

In addition, the United Arab Emirates imported 42,160 MT of alfalfa hay during the month, its highest total since December 2013. Despite those larger shipments to the Middle East, however, year-to-date U.S. alfalfa exports remained behind the record pace set in 2017.

Led by shipments to Japan and South Korea, U.S. exports of other hay held fairly steady in September, but remain on the slowest pace in well over a decade.

For the most part, threats of higher freight rates have not materialized.

Harvest delays and shrinking drought areas

A wet fall disrupted harvest in some regions of the U.S., and a surprising number of northern U.S. farmers attending the National Milk Producers Federation annual meeting, Oct. 28-31, said they were still trying to get hay off wet fields.

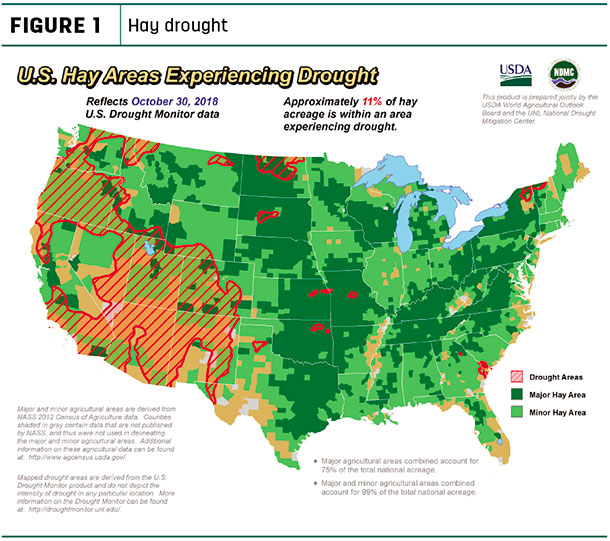

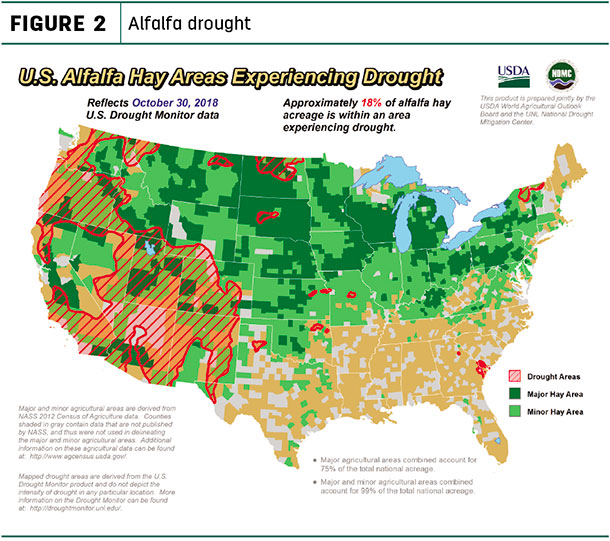

The wetter conditions were illustrated in the USDA World Agricultural Outlook Board’s latest drought maps. About 11 percent of U.S. hay-producing acreage was located in areas experiencing drought at the end of October (see Figure 1), down from 15 percent in early September and the smallest area since spring of 2017. Drought conditions all but disappeared in Texas, Missouri and Kansas during October. In alfalfa hay production areas, about 18 percent remained under drought conditions at the close of October (see Figure 2), also 4 percent less than the start of September.

Alfalfa hay prices halt slide

The latest available USDA monthly Ag Prices report summarized September 2018 prices.

Alfalfa

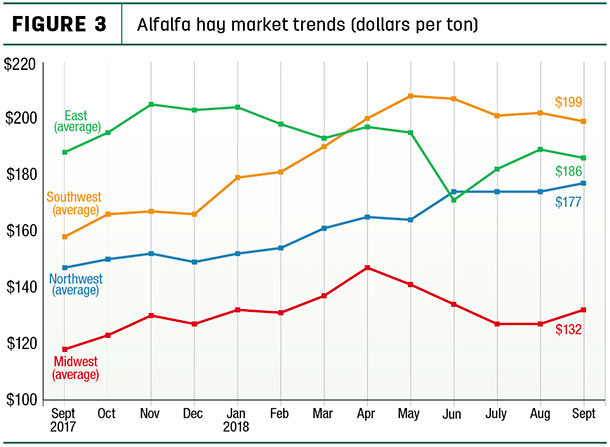

National average alfalfa hay prices ended a three-month downward trend. At $180 per ton, the September 2018 U.S. average price was up $3 from August and was $31 per ton higher than September 2017. Regionally, prices rose in the Midwest and Northwest, but were lower elsewhere (see Figure 3).

Compared to a month earlier, September average alfalfa hay prices rose $15 to $25 in Idaho, Minnesota and Wisconsin, but declined $10 per ton in Arizona, Montana, New Mexico and Ohio. Compared to a year earlier, alfalfa hay prices were up $50 or more per ton in Oregon, Kansas, Arizona and Oklahoma, with only North Dakota and New York reporting substantially lower prices than September 2017.

Alfalfa hay prices hit $230 in New Mexico and $220 in Kentucky, and were at $200 or more in Oregon, California, Arizona and Colorado. The low price for the month, at $88 per ton, could be found in North Dakota.

Other hay

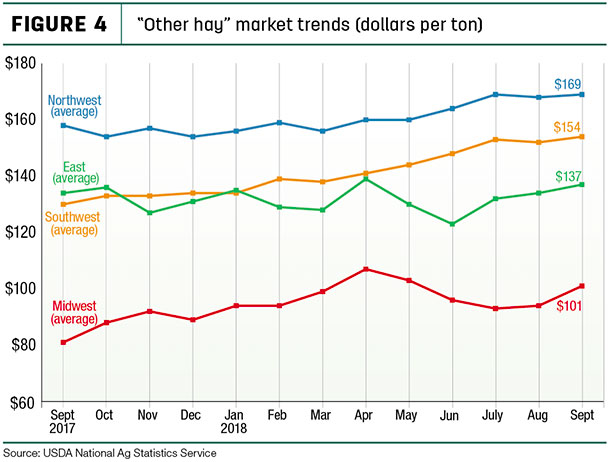

The U.S. average price for other hay was estimated at $130 per ton, unchanged from August and remaining at a 16-month high.

Looking at regional breakouts, September 2018 average prices were higher everywhere (see Figure 4). Among individual states, Wisconsin and Pennsylvania saw the largest monthly increases, up $29 and $25 per ton, respectively. Price declines of $8 to $10 per ton were seen in New York, Oklahoma, Michigan and Montana.

Highest average prices for other hay again hit $200 or more per ton in Arizona and Colorado. North Dakota and Minnesota saw monthly lows of $68 and $80 per ton, respectively.

Figures and charts

The prices and information in Figure 3 (alfalfa hay market trends) and Figure 4 (“other hay” market trends) are provided by NASS and reflect general price trends and movements. Hay quality, however, was not provided in the NASS reports. For purposes of this report, states that provided data to NASS were divided into the following regions:

- Southwest – Arizona, California, Nevada, New Mexico, Oklahoma, Texas

- East – Kentucky, New York, Ohio, Pennsylvania, Tennessee, Virginia

- Northwest – Colorado, Idaho, Montana, Oregon, Utah, Washington, Wyoming

- Midwest – Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, South Dakota, Wisconsin

Organic hay

According to the USDA’s organic hay report, f.o.b. farm gate prices at the end of October were:

- Supreme alfalfa small square bales – $265 per ton

- Premium-Supreme alfalfa large square bales – $260 per ton

- Premium alfalfa mid square bales – $200 per ton

- Good alfalfa mid square bales – $155 per ton

No price reports were available for delivered organic hay.

Dairy cow numbers coming down

The most striking numbers in the USDA’s monthly Milk Production report related to the size of the U.S. herd, which was retroactively reduced for June, July and August. With preliminary September estimates now available, U.S. cow numbers totaled 9.367 million head, down 32,000 head from a year earlier and the lowest total since February 2017.

Eight states increased cow numbers compared to September 2017, led by Texas, Colorado and Kansas. California, Ohio and Pennsylvania led decliners, with cow numbers also down a combined 16,000 head in Michigan, Minnesota and Wisconsin.

September U.S. average dairy income margins rose above USDA Margin Protection Program for Dairy (MPP-Dairy) payment trigger levels. Although nothing to write home about, current income margins are now expected to remain steady through July 2019.

The adverse economic conditions and herd liquidations continue to apply downward pressure on prices paid for dairy replacement cows. Preliminary October 2018 U.S. quarterly replacement dairy cow prices averaged $1,230 per head, $380 (24 percent) less than October 2017 and $890 (42 percent) less than the latest peak in October 2014. Average prices could be even lower, if not for a lower-valued portion of liquidated herds being sent directly to slaughter instead of being offered on the dairy replacement market.

Regional markets

Nevertheless, some regional hay markets reported improved dairy activity, although the trend was spotty. State conditions and market summaries as of late October follow:

-

Midwest: In Kansas, fields were drying up enough for farmers to finish harvest and start deliveries.

In Missouri, there was a lot of fall hay baled, which helped overall supplies. Improved water supplies allowed some to stockpile some grass, and many cattle farmers were waiting to see when snow falls before buying more hay.

Demand and prices moved higher in Nebraska, with demand from Colorado feedlots and dairies driving markets in the western part of the state. Producers were also baling cornstalks and soybeans.

Iowa weather has been tough on growers. Some producers managed to bale a fourth cutting; although sparse, it was some of the better hay baled this year. Those with better quality hay appear to have it in storage, waiting for higher prices. With limited supplies, those seeking high-quality hay have moved to “hand-to-mouth” buying.

In South Dakota, there was good demand for all qualities of alfalfa, and very good demand for high-quality grass hay. Dairymen continued their search for high-quality hay, but income margins were making them reluctant buyers.

In southwest Minnesota, prices were steady with no top-quality hay available.

In Wisconsin, quality alfalfa hay was in demand. Wet weather delayed fall harvest operations. Colder weather and some snow may motivate farmers to purchase hay in the near future.

-

Northwest: In Colorado, rain has helped improve both short- and long-term moisture deficits.

Demand picked up in some reporting areas of Wyoming. Large square bales of alfalfa were going to dairies in Texas. Some producers were working on the third and fourth cuttings of hay; others were done and had cleaned and put away their haying equipment.

Many Montana ranchers have moved cattle to market, freeing up funds to purchase hay for winter. Demand for dairy-quality hay was mostly moderate to good, with dairies in Washington and Idaho active market participants. Demand for hay moving to Colorado and other Southern drought states continues to be good. Outstanding weather to end October helped producers taking a third cutting.

In Idaho, some weakness was noted on Supreme alfalfa from dairies.

In Oregon, retail/stable-type hay remained most in demand. In the Columbia Basin, trade was very slow as exporters and dairies ship previously purchased supplies, and producers who have hay left were in no hurry to sell.

Utah hay prices were mostly firm, with trading slow on all qualities. A majority of movement was previously contracted hay.

-

Southwest: Alfalfa trade was slow in Oklahoma; the bulk of interest came from feedlots and cattle growing yards. Demand from dairies remained very light. Grass hay demand was also fairly limited, and buyers were very selective for quality and condition of grass hay.

In Texas, hay movement was hampered by muddy conditions. Some coastal bermuda producers in South Texas were able to get into their fields to bale the fourth cutting.

-

East: News out of the East has been light. Trade, supply and demand were all moderate in Alabama.

Market activity was light in the Lancaster area of Pennsylvania.

Other market factors

-

Fuel prices: The U.S. Energy Information Administration’s latest analysis anticipates planned fourth-quarter refinery maintenance shutdowns should have little impact on fuel supplies.

At $2.81 per gallon, the national average regular gasoline retail price ended October 32 cents higher than a year earlier, with substantially larger increases in the Rocky Mountain and West Coast regions.

At $3.36 per gallon, the U.S. average diesel fuel price was up 54 cents from a year earlier. California diesel prices were up almost 89 cents compared to a year ago.

-

Interest rates: Farm lending increased sharply in the third quarter of 2018, with much of the jump attributed to larger loans to cover operating expenses. The increase in the size of loans also boosted the share of agricultural lending at large banks, according Ty Kreitman, assistant economist in the Federal Reserve Bank’s Kansas City district.

Interest rates on farm loans continued to trend upward in the third quarter of 2018 on all loan sizes. For example, interest rates on variable-rate operating and intermediate loans in the Federal Reserve Bank of Dallas were the highest since 2008; interest rates on fixed-rate operating and intermediate loans are the highest since the end of 2011.

-

Dave Natzke

- Editor

- Progressive Forage

- Email Dave Natzke