The hay bales are wrapped and all nestled in sheds, while supply chain distractions bounce around in our heads. You get the picture. Here’s a look at forage market conditions entering the second week of December.

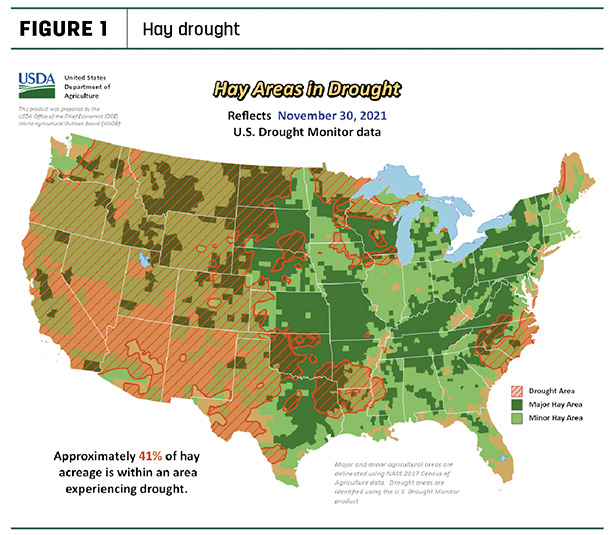

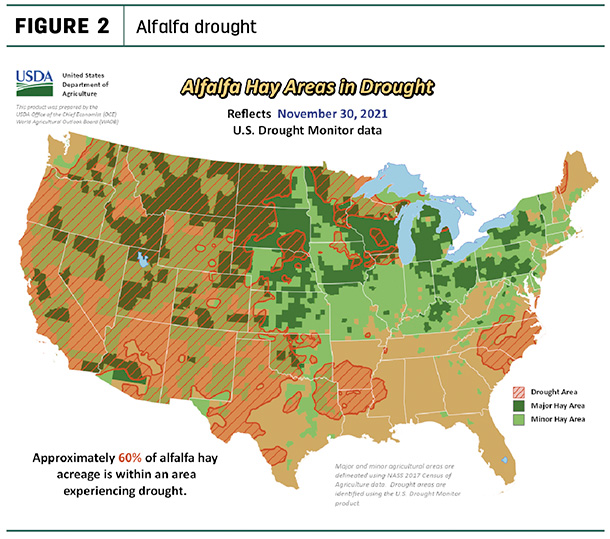

Drought conditions spread

Although harvest season is over, drought conditions in major forage areas worsened heading into winter. U.S. Drought Monitor maps estimated about 41% of U.S. hay-producing acreage (Figure 1) was considered under drought conditions, up 6% from the end of October. The area of drought-impacted alfalfa acreage (Figure 2) increased 2% over the previous month to 60%. In addition to long-term dry conditions in the West, drought areas spread in Texas, Oklahoma and portions of the Southeast, with only slight improvements in eastern North Dakota and northwest Minnesota.

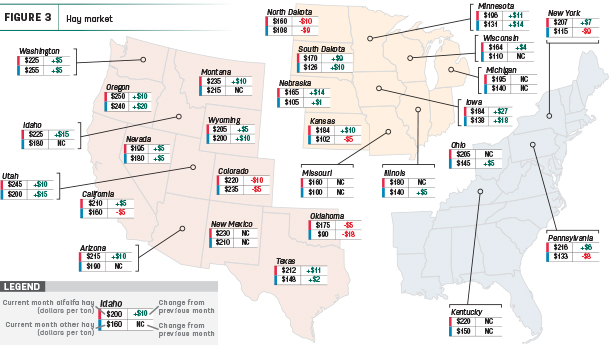

Alfalfa hay prices continue to climb

Price data for 27 major hay-producing states is mapped in Figure 3, illustrating the most recent monthly average price and one-month change. The lag in USDA price reports and price averaging across several quality grades of hay may not always capture current markets, so check individual market reports elsewhere in Progressive Forage.

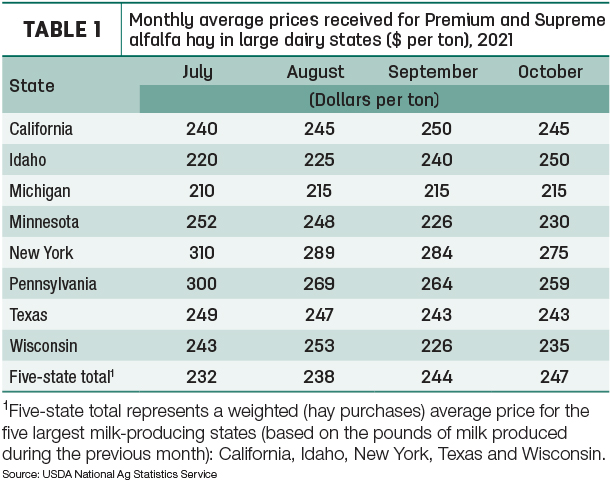

Dairy hay

The average price for Premium and Supreme alfalfa hay in the top milk-producing states rose $3 from September to $247 per ton (Table 1). October’s average is up $53 per ton from a year ago and is the highest average recorded since the USDA began compiling dairy-quality hay prices in 2019.

Compared to a month earlier, higher prices in Idaho, Minnesota and Wisconsin offset price declines in California, New York and Pennsylvania. Dairy-quality alfalfa hay prices were steady in Michigan and Texas.

Alfalfa

The national average price for all alfalfa hay rose for an 11th consecutive month in October, up $4 per ton from September to $213 per ton. It’s the highest monthly U.S. average dating back to July 2014. Monthly prices increased in 18 of 27 major forage states, with double-digit increases in 10 states and led by Iowa, up $27 per ton. Average prices declined in in just three states: Colorado, North Dakota and Oklahoma.

Other hay

The U.S. average price for other hay held steady in October at $145 per ton, maintaining a four-month low. Compared to September, average prices moved higher in 12 of 27 major hay-producing states. Largest increases were in Oregon, Iowa, Utah, Minnesota, Wyoming and South Dakota. Other hay prices were lower in seven states, led by Oklahoma, New York and North Dakota.

Organic hay

The USDA’s latest National Organic Grain and Feedstuffs Reports summarized recent prices paid for organic hay. For the two-week period ending Dec. 1, premium large square bales of alfalfa averaged $260 per ton. Prices listed are free on board (f.o.b.) farm gate.

Exports remain strong but challenges do too

Hay exporters remain frustrated over logistical challenges, although a review of USDA Foreign Ag Service (FAS) data shows alfalfa hay exports totaled 259,801 metric tons (MT) in October, up about 5,000 MT from September and the third-highest monthly total of the year. Sales to China totaled 162,856 MT, representing 63% of all alfalfa hay exports during the month. Shipments to Japan, South Korea, United Arab Emirates (UAE) and Taiwan were all up from September.

With shipping adding to costs, the USDA estimated the value of October alfalfa hay exports averaged about $377 per MT, up about $17 from September’s average.

January-October 2021 alfalfa hay exports total nearly 2.41 million MT, the highest volume on record for the first 10 months of the year.

In a separate report, the FAS said China’s demand for dairy products is driving milk production expansion and with it the use of high-quality alfalfa, timothy hay and oat grass. China imported 1.16 million tons of alfalfa hay in the first nine months of 2021, with the U.S. accounting for about 84% of that total. The average cost, insurance and freight price of U.S. alfalfa hay was $379.58 per ton over that period.

At 119,578 MT, October exports of other hay hit a five-month high, with larger shipments compared to a month earlier to Japan, South Korea, Taiwan and UAE. Shipments to Japan increased to 61,518 MT, but its percentage of all other hay exports fell to about 51% for the month. Year to date, Japan has been the destination for about 60% of all other hay shipments.

The USDA estimated the value of October other hay exports averaged about $362 per MT, $3.30 more than the September average.

Year-to-date exports of other hay have now topped 1.17 million MT, up about 52,000 MT compared to January-October 2020 and the largest volume for that period since 2016.

Despite the strong hay export totals, port data shows that port efficiency has deteriorated heading into the final two months of the year, according to the U.S. Dairy Export Council. Even though there was a slight improvement in October compared to September, 68% of all containers exported out of the ports of Los Angeles, Long Beach, Oakland and Seattle-Tacoma were empty.

Fundamentally, the major West Coast ports processed fewer containers (of all types) in October, likely because of challenges with securing trucking to move imported containers, equipment shortages and lack of available space at ports to offload imported products.

On a daily basis, the major West Coast ports processed the fewest inbound containers since January and 80,000 fewer containers than October of last year. The story was similar with outbound containers as well (regardless of whether they were loaded or empty).

On the positive side, spot shipping rates from Asia to the U.S. have started to decline, and the backlog of ships waiting outside the major California ports is starting to slowly shrink.

Regional markets

Here’s a snapshot of local markets:

- Southwest: In Texas, prices were steady in all regions, with trade activity and demand moderate. Dry conditions persisted in the Panhandle, west and central regions. Excessive moisture continues in the south, hampering producers trying to get a final cutting.

In Oklahoma, hay movement was beginning to pick up.

In California, hay trading remained steady with firm prices. Retail hay prices were steady to $5 higher. Dairy hay prices were steady to firm.

- Northwest: In Montana, hay sold fully steady with very good demand. Very few producers had hay left to sell. Producers and traders buying hay out of Canada report that supplies have started to tighten.

In Idaho, domestic alfalfa and wheat straw sold firm in a light test. End users are looking to supplement high-priced grain and hay.

In Colorado, horse hay sold steady on good demand. Trade activity was lighter for ranch hay, inactive on other markets.

In the Columbia Basin, domestic and export alfalfa and timothy sold firm in a light test. Most supplies were already spoken for.

In Wyoming, pellet prices in the east remained steady while hay trade was inactive. In western Wyoming, trade was light on good demand.

-

East: In Pennsylvania, buyer attendance at hay auctions was moderate to good. Alfalfa sold mostly steady, with alfalfa-grass blends selling firm on a light test.

- Midwest: In Nebraska, trade activity and demand were moderate, with alfalfa prices steady. Hay producers are expecting trade to pick up as winter weather arrives.

In Kansas, the south-central region seemed to have an undertone of softness to the market. In other regions, pricing remained firm, with concerns of higher operating costs next year and worsening drought.

In South Dakota, all classes of hay sold firm on good demand. Demand was very good for high-quality alfalfa.

In Missouri, the supply of hay was moderate, demand was light to moderate, and prices were mostly steady. Farmers were starting to feed a little hay as stockpiled pastures dwindled, but milder temperatures kept feeding needs lower.

In Iowa, buyer demand was good; alfalfa sold steady with a weak undertone, while grass sold $1-$4 higher.

Other things we’re seeing

- Dairy: Offsetting the higher alfalfa hay prices, U.S. milk producers got some feed cost relief from lower corn and soybean meal prices in October. However, that didn’t stop the downward trend in cow numbers. Dairy cow numbers declined for a fifth consecutive month, down 14,000 from both September 2021 and October 2020. Since peaking in May 2021, U.S. cow numbers were down 107,000 head and the lowest in more than a year. In a continuing trend, the USDA’s World Ag Supply and Demand Estimates (WASDE) report reduced milk production forecasts and raised projected milk prices for both 2021 and 2022.

The USDA finally announced details regarding hay price calculations used in the Dairy Margin Coverage (DMC) program that will provide retroactive indemnity payments for 2020-21.

-

Beef cattle: Depopulation of U.S. beef cattle accelerated this year due to poor economics and drought liquidation across the West. Beef and dairy cow slaughter increased by 6%, which will lead to a 2.5% decline in U.S. beef production in 2022, according to a recent report from Rabobank.

-

Fuel and trucking: Crude oil spot prices fell during the week ending Dec. 1 in response to expectations that the omicron variant of COVID-19 could reduce global petroleum demand. In its December Short-Term Energy Outlook report, the U.S. Energy Information Administration revised global demand in the first quarter of 2022 to reflect that potential decrease in demand. National average flatbed hauling rates increased slightly ($3.04 per mile) to end November. Highest rates were in the Midwest and Southeast.

-

Fertilizer: CoBank’s Knowledge Exchange reports a dramatic rise in fertilizer prices is weighing heavily on U.S. crop farmers and input suppliers as they prepare for the 2022 planting season. Fertilizer prices are expected to remain elevated for at least the next six months and throughout the 2022 spring agronomy season.