Whole Farm Revenue Protection (WFRP) insurance was created by the Agricultural Act of 2014. It has been available for purchase since the 2015 crop year. Since then, each year has brought updates to the program.In 2016, the USDA Risk Management Agency expanded WFRP availability to every county in the nation.

The 2016 crop year brought increased access to WFRP for beginning producers, increased coverage limits for livestock producers and increased ability to cover expected growth in operations and sales. The 2018 crop year brings only minor adjustments to WFRP.

WFRP offers a risk safety net via a single insurance policy for the entire farm. It covers all commodities including livestock and specialty or organic crops. It covers up to $8.5 million of revenue. Coverage levels range from 50 up to 85 percent in 5 percent increments.

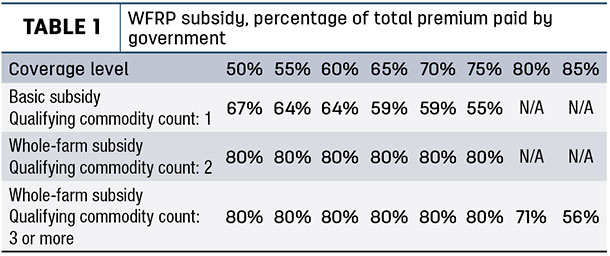

Premium subsidies range from 55 up to 80 percent of the total premium collected, depending upon coverage level and farm diversification (Table 1).

Farm diversification is rewarded in the form of a higher subsidy level because the farm is pooling production and market risk across multiple commodities.

WFRP coverage is based on a Whole Farm History Report completed using five years of Internal Revenue Service – Schedule F or other farm tax forms. For the 2018 policy year, 2012 to 2016 tax forms are required. Unless an operation is a late-fiscal-year filer, sales closing dates for WFRP are the same as other spring crop sales closing dates applicable for the county and were on Jan. 31, Feb. 28 and March 15.

New for 2018, late-fiscal-year filers now have a sales closing date of Nov. 20 for WFRP. An Intended Farm Operation Report is completed at the time of enrollment to outline intended production plans; a Revised Farm Operation Report is due for all insured commodities on July 15 to update production plans; premiums are due August 15.

Late-fiscal-year filers previously followed alternative due dates for the Revised Report and premiums; for 2018 and beyond, that is no longer the case.

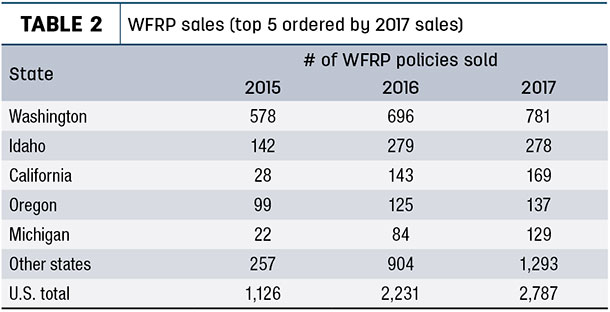

Since its inception, WFRP has been most popular in the Northwest U.S. and California, but sales have been growing throughout the U.S. (Table 2).

WFRP is well-suited for highly diversified farms selling into specialty markets or via direct sales in farm identity-preserved markets. These farms typically receive a premium for their product without available commodity-specific insurance.

Other situations where WFRP may be a good fit include organic production or specialty-crop sales where quality is rewarded in the marketplace – for example, hay producers that sell directly to a dairy at a premium price for high-quality hay meeting specific standards.

The Expected Value section of the policy is used to establish the price anticipated for each commodity, including marketing contracts and past sales history. New for 2018, if a marketing contract becomes effective after the Intended Farm Operation Report is submitted, the Expected Value may be revised to reflect the price contained in the marketing contract for the portion of production under contract.

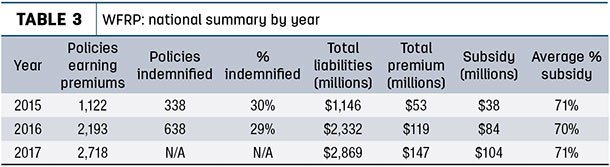

For 2015 and 2016, about 30 percent of WFRP policies earning a premium have been indemnified, with a loss ratio running about 30 percent above the total premium collected (Table 3).

Nationally, WFRP premium subsidies have averaged about 70 percent. This indicates a large number of producers paying premiums have only had one commodity-to-count (Table 1).

The WFRP commodity count is based on reaching one-third of the revenue needed for perfect diversification. For example, a two-commodity farm with perfect diversification would receive 50 percent of its revenue from each commodity.

In order to count, each commodity must provide at least one-third of 50 percent of the revenue or 16.7 percent. In addition, commodities can be grouped together to reach that threshold. Thus, as long as a single commodity does not account for more than 83.3 percent of the revenue, it is possible to group together expected revenue from several other commodities-to-count as the second commodity.

For example, consider a cattle and hay operation with a whole-farm historical average revenue of $260,040, based on the five consecutive tax years prior to the policy year. Where cattle prices are down slightly compared to the five-year average, the calculated total expected revenue for the coming policy year is $242,310 for this operation.

The farm raises high-quality grass hay. However, the expected total revenue from hay sales is only $9,800 because most of the hay raised is fed to the cattle. The remaining $232,510 in expected revenue is all generated by calf sales. Where calf sales constitute 96 percent of expected revenue, this would be classified as a one-commodity farm for WFRP coverage. The farm may insure expected whole-farm revenue at a coverage level between 50 and 75 percent, with an associated basic premium subsidy between 67 and 55 percent (see Table 1).

Now consider a similar cattle and hay operation that typically ships a large quantity of its high-quality grass hay to a regional metropolitan area for sale at a premium to horse owners. Revenue is generated in exchange for increased expenses associated with shipping the hay and purchasing feed to replace it. The whole-farm historical average revenue for this operation is $314,044.

The calculated total expected revenue for the coming policy year is $292,620. The expected revenue from calf sales is $232,510, just as in the preceding example. However, the expected revenue from hay sales is now $60,110. Where hay sales now comprise 20.5 percent of expected revenue, this second operation would have two commodities-to-count for WFRP coverage.

As a result, the premium subsidy for WFRP coverage would be 80 percent for all coverage levels between 50 and 75 percent.

The commodity count is one of several calculations to determine how well WFRP fits the unique situation of each farm or ranch operation. Producers interested in WFRP insurance for 2018 should visit the Risk Management Agency website (www.rma.usda.gov) and contact a crop insurance agent for details. ![]()

The authors are part of the RightRisk.org team: Jay Parsons is an associate professor with the University of Nebraska – Lincoln; John Hewlett is a ranch/farm management specialist with the University of Wyoming; Jeff Tranel is a business management economist with Colorado State University.

Jay Parsons is an associate professor with the University of Nebraska – Lincoln. Email Jay Parsons.