Alfalfa hay prices lowest since February 2011

National average alfalfa hay prices continued their downward spiral, according to the USDA National Ag Statistics Service’s (NASS) monthly Ag Prices report, released Dec. 29.

Alfalfa

The November 2016 U.S. average price paid to alfalfa hay producers at the farm level was $130 per ton, down $5 from October and $17 less than a year earlier. Except for a small increase in March-April, 2016 alfalfa hay prices have been less than the previous month in nine of the past 11 months, and are at the lowest level in 70 months.

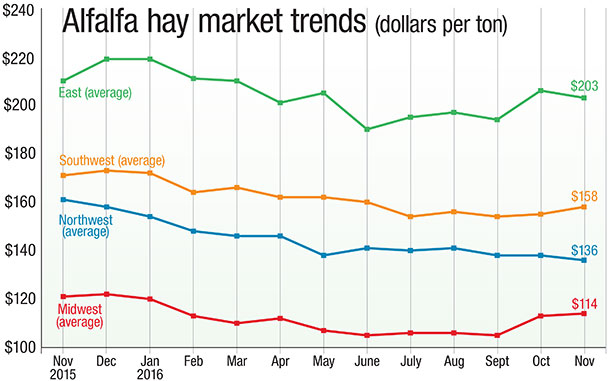

Despite the overall national decline, November prices were up about $3 per ton in the Southwest (Figure 1) compared with October, with the monthly increases in Nevada (up $10), Texas (up $6) and Arizona (up $5) offsetting declines in Oklahoma (down $5).

Compared with October, November prices were about steady to lower in other regions of the country. Michigan saw a $10 per ton increase, while its neighbor, Wisconsin, saw a $17 per ton decline. The average November price in Pennsylvania was down $8 per ton.

Most states saw alfalfa hay prices lower than a year ago, with prices in Idaho, Oregon and Pennsylvania down $55 to $61 per ton.

Kentucky continued to be the price leader in November 2016 at $225 per ton, with New York also topping the $210 per ton mark. Lowest average prices were in Nebraska ($79 per ton), North Dakota ($84 per ton) and South Dakota ($92 per ton).

Other hay

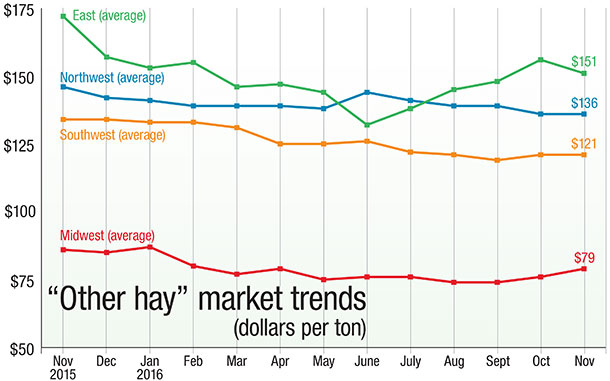

The November U.S. average price for other hay was estimated at $123 per ton, up $2 from October but $1 less than November 2015. Regional averages were up in the East and Midwest, but unchanged in the Northwest and Southwest (Figure 2).

Among individual states, producers in Wisconsin saw a $19 per ton increase compared with a month earlier, while Kansas, New York, Ohio and Oregon posted declines of $10 to $13 per ton.

Compared with a year earlier, other hay prices were down $40 to $60 per ton in Arizona, Nevada, Oregon and Pennsylvania, but up $26 per ton in Texas.

Highest November 2016 prices were in Pennsylvania ($188 per ton) and New York ($185 per ton); lowest prices were in Minnesota ($55 per ton), Kansas ($65 per ton) and North Dakota ($67 per ton).

Organic hay

Large square bales of California- and Oregon-sourced premium and supreme quality hay sold in a range of $250-$315 per ton (FOB the stack or barn) for the two-week period of Dec. 8-21, according to USDA’s bi-weekly organic feedstuffs report. Supreme alfalfa/grass large square bales brought $280 per ton, with fair/good quality alfalfa/grass bales averaging $200 per ton.

California decline continues

Driven by low commodity prices and a weaker dairy sector, alfalfa hay prices were quite painful for alfalfa producers in 2015-2016, according to Dan Putnam, forage agronomist with the University of California – Davis Extension.

While high-quality hays still fetched good prices, prices for lower-quality hays often were $80 to $100 per ton lower than high-quality alfalfa due to high supplies and lack of demand.

At the farm, the hay industry in California was worth between $1.5 billion and nearly $1.8 billion in 2011-2015, but is likely to be lower than this in 2016 due to low prices and reduced acreage. California alfalfa acreage has slipped from a peak of 1.1 million acres eight years ago to the current level of between 820,000 to 860,000 acres, Putnam said.

Auction and market summaries

December hay auction and market reports were limited due to the holidays, with regular schedules resuming in early to mid-January. Based on summaries of reports issued prior to the Christmas holiday:

• Southeast: Alabama hay prices were mostly steady on moderate trade, with moderate supply and good demand.

• Southwest: In Utah, prices were mostly steady to weak, with trading slow for all qualities of hay. In Oklahoma, demand was moderate for alfalfa and wheat hay, very light for other offerings. Most of the state is now in abnormally dry condition, and some areas are entering extreme drought status. In Texas, hay prices were mostly steady on light to moderate movement. Top quality alfalfa continued to hold steady, as freight charges played a factor. In California, all classes traded steady with moderate demand.

• Northern Plains: In South Dakota, the market was steady to weak. Alfalfa quality was average, while grass was mostly fair. Demand was good for immediate needs, while contracts continue to be very slow. Interest continues to be lighter than normal as cattle and milk prices are below break-even prices. In Montana, alfalfa hay sold generally steady; demand was moderate to good. With the onset of winter weather, feeders were buying last-minute loads to cover needs.

• Central Plains: Demand for hay has picked up in Nebraska; however, hay sold unevenly steady. Adequate supplies provided resistance to an increase in prices. Ground and delivered hay and dehydrated pellets sold steady. Alfalfa and grass hay demand picked up, mostly due to the sharply lower temperatures. Backgrounding lots and feedyards are starting to utilize more roughage. In Kansas, winter storms encouraged more hay feeding. Trade remained moderate with prices generally steady.

• Northwest: In Idaho, feeder grade alfalfa and export quality timothy hay prices were steady in a light test. Trade remains slow with light to moderate demand. In Washington and Oregon’s Columbia Basin, all grades of export and domestic alfalfa hay were weak in a light test. Trade was slow with light to moderate demand. Some producers and exporters are liquidating hay supplies to generate cash flow. In Oregon, demand was strongest for retail/stable hay.

• Midwest: In Illinois, hazardous weather affected auction sales; demand was light to moderate. In Iowa, demand was mixed with prices mostly steady. Supplies remain adequate. High-quality hay continues to bring a premium. In Wisconsin, large volumes of lower quality hay influenced the market. In Missouri, hay feeding is on the rise, but hasn’t reached its peak. Hay supplies are moderate, with demand light and prices mostly steady.

• Northeast: In Pennsylvania, all hay varieties sold mostly steady. Straw traded with a weaker undertone. In the Lancaster area, supplies were heavy in an effort to move hay before the end of the year. Large squares of alfalfa and grass hays sold mostly steady. Small squares sold with a weaker undertone, with exception of premium quality hays, which sold steady. Demand was good on an active trade.

Drought areas

Winter precipitation is helping improve drought conditions in some hay-producing areas, according to USDA’s World Agricultural Outlook Board weekly update. As of Dec. 27, about 24 percent of U.S. hay acreage was located in areas experiencing drought, down 8 percent from earlier in the month. Improved moisture conditions were reported in Oregon, Kentucky and Tennessee.

Check out the hay areas under drought conditions.

Hay exports

At 206,249 metric tons (MT), October marked the sixth consecutive month alfalfa hay exports have topped 200,000 MT.

Exports of other hay were down slightly from September, but still the second-highest volume in 2016.

Exports of dehydrated and sun-dried alfalfa cubes were down slightly from September. However, exports of all forms of alfalfa meal were up from the previous month. Dehydrated alfalfa meal exports were the highest monthly volume since November of 2008.

Looking ahead, China is likely to cut back on hay imports after declining milk prices forced dairies to cull heavier, according to Christy Mastin with hay exporter Eckenberg Farms Inc., Mattawa, Washington. Japan’s Hokkaido area, where many replacement heifers and forages are raised, was hit by heavy rains during the harvest season, boosting needs for purchased hay. The Japanese government is still supporting the use of domestic forage, and currency exchange rates remain a concern. The Hanjin shipping line bankruptcy kept a lot of cargo in Korea’s Busan port that otherwise would have been moved to other destinations.

Dairy outlook: Follow the cows

After a two-month decline, USDA estimated milk cow numbers increased slightly in November. Among the major dairy states, cow numbers grew in 11 states and declined in 11 others, with New York unchanged. Compared with a year earlier, November cow numbers were up 28,000 in Texas and 12,000 each in Idaho and Michigan. In contrast, cow numbers were down 11,000 in California.

According to Marvin Hoekema, president of Dairy Decisions Consulting LLC, the state cow numbers represent more of a relocation rather than outright expansion. Animals are moving from high-cost to low-cost feed areas. Specifically, animals are moving from California to Texas, Idaho and Kansas.

U.S. dairy cow numbers are expected to average 9.335 million head in 2016, and are forecast to rise throughout 2017, averaging 9.36 million head for the year. Despite that growth, the increase is slower than previously expected.

U.S. dairy product exports could top 17 percent of total production in 2016-2017, despite the headwinds of a strong U.S. dollar against other currencies. Combined with expected strength in domestic demand, USDA raised milk price projections to end 2016 and into 2017.

The midrange in the all-milk price forecast for the fourth quarter of 2016 is $17.15 per hundredweight (cwt), the highest quarterly average since the fourth quarter of 2015. The midrange forecast for the first quarter of 2017 is $17.50 per cwt.

Beef cattle outlook: More expected

The expected slower pace of cattle placements in late 2016 will cap beef production increases in the first half of 2017. However, supplies of slaughter-ready cattle are still expected to support a 3 percent increase in beef production over the period. Cattle prices in the first half of 2017 are expected to be more than 18 percent below the first half of 2016.

Steer price forecasts for the balance of 2016 and well into 2017 continue to reflect more-than-adequate supplies of cattle. Quarterly average prices for the fourth quarter of 2016 through the first half of 2017 are projected to be 17 to 21 percent less than the same period a year earlier.

Figures and charts

The prices and information in Figure 1 (alfalfa hay market trends) and Figure 2 (“other hay” market trends) are provided by NASS and reflect general price trends and movements. Hay quality, however, was not provided in the NASS reports.

For purposes of this report, states that provided data to NASS were divided into the following regions:

Southwest – Arizona, California, Nevada, New Mexico, Oklahoma, Texas

East – Kentucky, New York, Ohio, Pennsylvania

Northwest – Colorado, Idaho, Montana, Oregon, Utah, Washington, Wyoming

Midwest – Illinois, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, South Dakota, Wisconsin ![]()

-

Dave Natzke

- Editor

- Progressive Dairyman

- Email Dave Natzke