(Read also: Winter U.S. hay inventories smallest since 2012.)

Still to come, the USDA will issue its Prospective Plantings report on March 29, estimating potential alfalfa and other hay acreage for 2018.

Next month, Progressive Forage will provide its annual review of state-by-state hay, forage and silage production, new alfalfa seeding and more.

Alfalfa exports near annual record

Monthly alfalfa hay exports exceeded 200,000 metric tons (MT) in November, a 5 percent increase from October. Year-to-date 2017 alfalfa hay export sales topped 2.4 million MT and were just short of a new record annual high with one month to go on the 2017 export calendar.

November alfalfa hay exports totaled 202,869 MT, valued at about $59 million. China was the leading buyer with 81,932 MT, the largest total in three months.

Sales of other hay totaled nearly 133,000 MT, the fifth-highest monthly total of the year. Japan and South Korea remained top buyers. The other hay exports were valued at about $41.8 million.

Sales of alfalfa meal and cubes were consistent with previous months.

Post-holiday U.S. shipping schedules have returned to normal, although the West Coast has had some container shortages and vessel service changes, which has delayed vessels and caused more shifting of cargo, according to Christy Mastin, international sales manager at Eckenberg Farms, Mattawa, Washington.

Although December shipment totals haven’t been released, Mastin expects year-end exports to reflect a continuation of November’s strength, and overall alfalfa exports should remain at high levels. However, the Chinese New Year celebration is coming up in February, so January shipments could drop off.

The U.S. “other hay” markets in Japan and South Korea should also end the year strong, although timothy markets are currently slow in both countries due to large inventories in warehouses.

Straw has been in short supply because of reduced U.S. production. South Korea’s domestic harvest was stronger this year, but demand remains high.

“Overall the volume numbers were good for export of forage products,” Mastin said. “We hope that any political changes won’t adversely affect the trade and relationships that have been built over the years.”

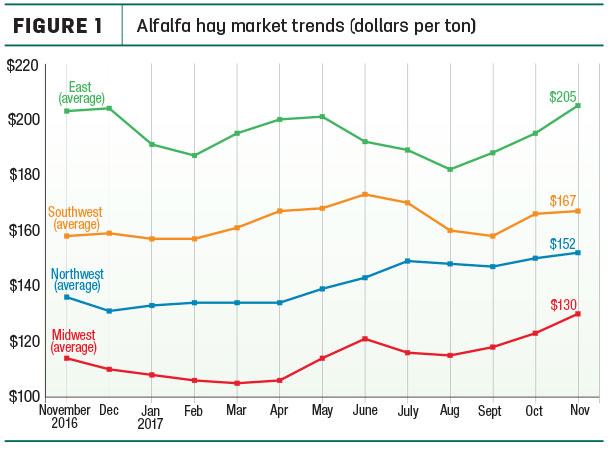

Alfalfa hay prices

The latest available USDA monthly Ag Prices report was released Dec. 28, summarizing November 2017 prices.

Alfalfa

The November 2017 U.S. average price paid to alfalfa hay producers at the farm level was $148 per ton, down $4 from October but $18 more than a year earlier.

The national average price belies changes in regional (Figure 1) and state prices. Only Kansas, Michigan and Nevada saw lower prices compared to October. Average prices did jump $25 to $27 per ton in New York, Minnesota and Iowa, and were $10 to $17 higher in Arizona, Pennsylvania and Wisconsin.

Highest alfalfa hay prices were in New York ($244 per ton), Arizona and Kentucky ($205 per ton); lowest prices were in Nebraska ($90 per ton) and North Dakota ($104 per ton).

Comparing November average to year-ago levels, there were wider swings among individual states. Prices were $25 to $40 per ton higher in Arizona, California, Colorado, Iowa, Kansas, Minnesota, New York and Wisconsin but $15 to $29 lower in Illinois, Kentucky, Missouri and Oklahoma.

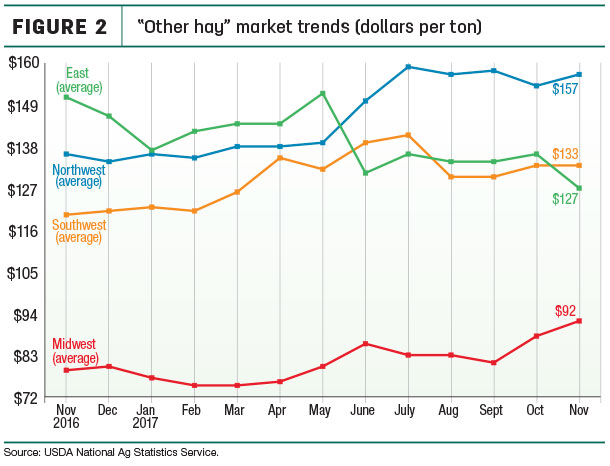

Other hay

The November 2017 U.S. average price for other hay was estimated at $118 per ton, unchanged from October and $2 per ton less than November 2016. Regionally, prices were lower in the Northeast (Figure 2). Among individual states, October prices for other hay were up $10 to $20 per ton in Iowa, Minnesota, Nevada, Oregon and Wisconsin but $20 lower in New York and North Dakota.

Highest other hay prices were in Washington ($190 per ton), Arizona and Colorado ($180 per ton); lowest prices were in Oklahoma ($65 per ton) and Nebraska ($73 per ton).

Compared to a year earlier, average prices for other hay were up $33 per ton in Wisconsin and $25 to $30 higher in Colorado, Minnesota, New Mexico, Oregon, Washington and Wyoming. In contrast, prices were $54 per ton lower in New York and down $25 per ton in Pennsylvania.

Figures and charts

The prices and information in Figure 1 (alfalfa hay market trends) and Figure 2 (“other hay” market trends) are provided by NASS and reflect general price trends and movements. Hay quality, however, was not provided in the NASS reports. For purposes of this report, states that provided data to NASS were divided into the following regions:

- Southwest – Arizona, California, Nevada, New Mexico, Oklahoma, Texas

- East – Kentucky, New York, Ohio, Pennsylvania

- Northwest – Colorado, Idaho, Montana, Oregon, Utah, Washington, Wyoming

- Midwest – Illinois, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, South Dakota, Wisconsin

Organic hay

The USDA’s Organic Hay report, released Dec. 20, reported grower FOB farm gate organic hay prices as follows: Premium alfalfa large square bales – $250 to $290 per ton. No prices were reported for delivered hay.

National organic grains and feedstuffs report

Regional auction and market summaries

Here’s a peek at mid-January auction market summaries:

- East: Alabama hay prices were fully steady, with moderate supply and good demand. In Pennsylvania’s Lancaster area, all varieties of hay and straw sold mostly steady with the exception of some firmness noted in small bales of grass hay. Supply was moderate. Demand was moderate.

- Southwest: All classes of California hay traded steady with moderate demand. Retail hay was in high demand due to lack of hay in barns this year. In Oklahoma, alfalfa trade and movement was slow to moderate. Demand was mostly good, but supplies were fairly tight.

Prices on dairy hay were fully steady, but bunk and dry cow hay was $5 to $10 higher. Wheat pasture conditions continue to deteriorate due to lack of moisture. Demand for grass hay has improved in central and western Oklahoma. Demand and movement in most eastern counties was light to moderate. In Texas, hay sold mostly steady to $5 to $10 higher. Demand continued to increase with the supply of hay decreasing. Wheat hay was difficult to find. Supplemental feeding of livestock remains in full swing across the state.

- Northwest: In Idaho, mudding conditions made trading slow. There was some interest in straw. In Oregon, prices trended generally steady in a limited test. Retail/stable type hay remained the most demanded hay. Sales of feeder alfalfa decreased. Many hay producers have sold out for the growing year. In the Washington-Oregon Columbia Basin, trade was slow with light to moderate demand.

Timothy for export remains slow; competition from Canadian timothy and Australian oat hay are hurting U.S. exporters. In Wyoming, alfalfa hay sold fully steady. Some hay was getting imported to ranchers in the northeastern side of the state. Also, large square bales of alfalfa hay were moving to dairies from Colorado to Texas. In Montana, hay prices were steady; demand was light to moderate.

Colorado prices were steady, with activity light and demand good in all classes. Prices were above normal for small squares of grass hay due to limited availability. Moderate drought conditions were expanded over all of eastern Colorado, with dryness over the last three months being a concern.

- Midwest: In Iowa, alfalfa and grass hay prices were steady, supported by increased demand from cattle feeders. Drought concerns were also adding to demand. In Missouri, hay supplies were moderate, demand was light to moderate, and prices were steady to firm. Interest in hay has picked up slightly with colder temperatures.

The best interest was for better-quality hay coming from horse owners, and prices have crept up slightly; supplies of that type of hay have become less abundant. Across Kansas, market activity was moderate; demand moderate to good for alfalfa and moderate for grass hay. Prices were steady to firm for all classes. The slowdown in hay movement during the Christmas holiday was short-lived, as wheat pasture was virtually nonexistent and feeder pens were full.

Grinding hay continues to be elusive, strengthening its price with an undertone of strength to the grass hay market. In Nebraska, prices were steady to $5 per ton stronger with moderate demand for all hay classes. In South Dakota, all classes of hay were steady to firm, with straw up $10. Cold and snow were driving the market, but there was still some resistance because of low grain prices.

Hay producers were sitting on hay rather than letting it go at the current price because of the dry conditions this past summer. In Wisconsin, there was some strength in the market across all classes of hay. There was a large demand for straw. In southwest Minnesota, hay supply was adequate; the price trend was steady with limited quality hay available. Straw was in demand this week.

Drought area

Winter is just getting started, but drought conditions are worsening. The USDA’s World Agricultural Outlook Board estimated 30 percent of U.S. hay-producing acreage was located in areas experiencing drought as of Jan. 9.

In addition to continuing dry conditions in Montana and western North Dakota and South Dakota, a large droughty swath now covers an area stretching from southern Illinois through major hay-producing sections of southeastern Missouri, Kansas, Arkansas, Oklahoma, Texas, New Mexico, Arizona, Utah and Colorado. Dry pockets are also in parts of Pennsylvania, Virginia North Carolina, Georgia, Iowa and southern California.

Check out the hay areas under drought conditions.

Fuel prices and outlook

The U.S. Energy Information Administration estimated U.S. retail prices for regular gasoline averaged about $2.52 per gallon during the first week of January, unchanged from the week before but 13 cents per gallon more than a year ago. The Energy Information Administration expects the retail price of regular gasoline to average $2.51 per gallon during the first quarter of 2018, 19 cents gallon higher than at the same time last year, primarily reflecting higher crude oil prices.

U.S. on-highway diesel fuel prices averaged about $3.00 per gallon, up 2.3 cents from a week earlier, 40 cents per gallon more than a year ago. The diesel price is forecast to average $2.95 gallon in 2018 and $3.01 per gallon in 2019, driven higher primarily by higher crude oil prices and growing global diesel demand.

Dairy outlook: A tough start to the year

November 2017 U.S. milk production grew just 1 percent compared to the same month a year earlier, with weak growth in milk output per cow applying most of the brakes. Nationally, cow numbers remained at a six-month low.

Nationally, November milk cow numbers were unchanged from October but 57,000 head more than November 2016. Compared to a year earlier, largest growth was in Texas (+25,000 head), Arizona, Colorado (each +9,000 head) and New Mexico (+6,000 head). California (-14,000 head) and Minnesota (-4,000 head) led decliners.

Despite the modest growth in milk production, prices are expected to be weaker. USDA projections put the 2017 all-milk price at $17.65 per hundredweight (cwt), falling to about $16.20 per cwt in 2018. The USDA-projected 2017 Class III price is about $16.17 per cwt, dipping to $14.65 per cwt in 2018. The projected 2017 Class IV price is $15.16 per cwt, weakening to $14 per cwt in 2018.

Beef outlook: First quarter will be strongest

The USDA’s 2018 beef production forecast was raised as higher cattle placements in late 2017 are expected to result in higher fed cattle marketings and slaughter in the first half of 2018. Average carcass weights are also expected to be heavier. The projected 2018 cattle price is down slightly from 2017, with strongest prices in the first quarter of the year. ![]()