Read also: Western hay market outlook for 2018.

The next USDA reports monitoring supply include an inventory report on Jan. 12, providing an estimate of hay in storage on farms as of Dec. 1. The Jan. 12 Crop Production report traditionally estimates the number of acres of alfalfa newly planted in 2017. Then the USDA will issue its Prospective Plantings report on March 29, estimating potential alfalfa and other hay acreage for 2018.

Hay exports holding up

Monthly alfalfa hay exports dipped below 200,000 metric tons (MT) in October, the fourth time that’s happened in the past 18 months. Despite the slight downturn, year-to-date 2017 alfalfa hay export sales topped 2 million MT and remain well on their way to a new record annual high.

October alfalfa hay exports totaled 192,552 MT, valued at about $57 million. China was the leading buyer with 75,033 MT, although shipments declined for a second consecutive month.

Sales of other hay totaled nearly 135,056 MT, the fourth-highest monthly total of the year. Japan and South Korea remained top buyers. The other hay exports were valued at about $42.6 million.

A couple of factors will impact hay exports as 2017 comes to a close, according to Christy Mastin, international sales manager at Eckenberg Farms, Mattawa, Washington. November and December holidays reduce the number of U.S. shipping days, and the Chinese New Year celebration causes a month-long slowdown for incoming shipments. Shipments had to leave U.S. ports by mid-December to arrive before the Chinese new year.

Demand for higher-quality alfalfa has been steady from Japan and South Korea. Although domestic hay harvest was better than last year, overall hay quality isn’t back to normal. Japan and South Korea also have large inventories of timothy that will be fed through the winter, so U.S. shipments could pick up in 2018.

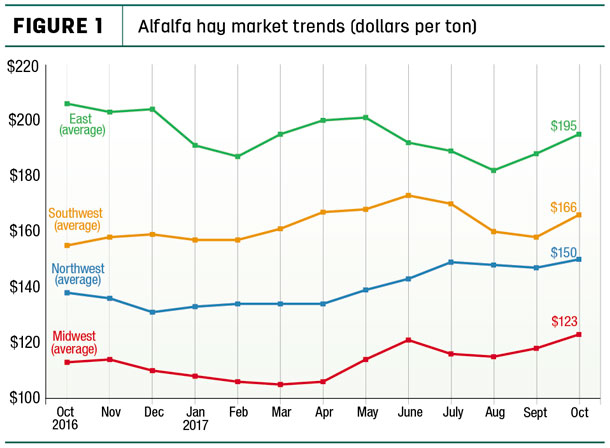

Alfalfa hay prices

The latest available USDA monthly Ag Prices report was released Nov. 30, summarizing October 2017 prices.

Alfalfa

The October 2017 U.S. average price paid to alfalfa hay producers at the farm level was $152 per ton, up $3 from September and $17 more than a year earlier.

October prices were steady to higher than month-earlier levels in most of the country (see Figure 1), with only a handful of states reporting price declines.

Among individual states, prices were up $15 to $30 per ton in California, Michigan, New York and Oregon, but down $5 per ton in Idaho, North Dakota, Washington and Wisconsin. Highest alfalfa hay prices were in New York ($219 per ton) and Kentucky ($205 per ton); lowest prices were in Nebraska ($96 per ton) and Iowa ($106 per ton).

Compared with a year earlier, only the East saw lower average prices. There were wide swings among individual states. Prices were $20 to $35 per ton higher in Arizona, California, Colorado, Kansas, Nevada, New Mexico and North Dakota, but $15 to $40 lower in Illinois, Kentucky, Missouri, Oklahoma and Pennsylvania.

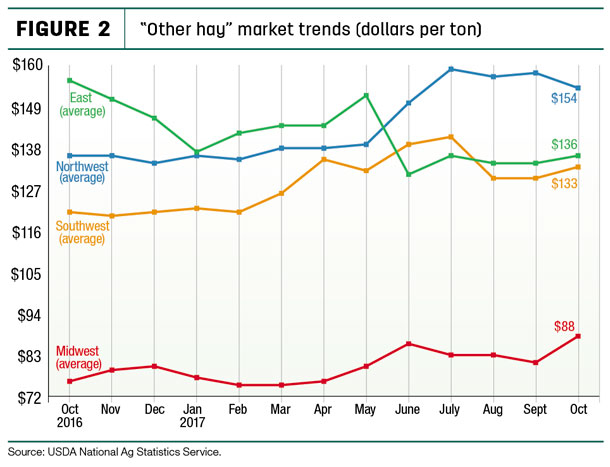

Other hay

The October 2017 U.S. average price for other hay was estimated at $118 per ton, up $5 per ton from September and moving off a 12-month low. Regionally, prices were mixed, higher in the Midwest but lower in the Northwest (see Figure 2).

Among individual states, October prices for other hay were up $10 to $22 per ton in Arizona, Kansas, Michigan, Ohio, South Dakota and Wisconsin, but $10 to $20 lower in Oregon and Washington. Highest other hay prices were in Washington ($190 per ton) and Arizona ($180 per ton); lowest prices were in Minnesota ($69 per ton) and North Dakota ($70 per ton).

Compared with a year earlier, average prices for other hay were up $41 per ton in Wisconsin and $30 to $35 higher in New Mexico, Washington and Wyoming. In contrast, prices were $46 per ton lower in New York and down $24 per ton in Pennsylvania.

Figures and charts

The prices and information in Figure 1 (alfalfa hay market trends) and Figure 2 (“other hay” market trends) are provided by NASS and reflect general price trends and movements.

Hay quality, however, was not provided in the NASS reports. For purposes of this report, states that provided data to NASS were divided into the following regions:

- Southwest – Arizona, California, Nevada, New Mexico, Oklahoma, Texas

- East – Kentucky, New York, Ohio, Pennsylvania

- Northwest – Colorado, Idaho, Montana, Oregon, Utah, Washington, Wyoming

- Midwest – Illinois, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, South Dakota, Wisconsin

Organic hay

The USDA’s Organic Hay report, released Nov. 22, reported grower FOB farm gate organic hay prices as follows: Premium alfalfa small square bales – $265 per ton; Premium alfalfa-grass small square bales – $240 per ton. Good wheat large square bales – $175 per ton; and Good/Premium triticale large square bales – $140 per ton. No prices were reported for delivered hay.

National organic grain and feedstuffs report

Regional auction and market summaries

Here’s a peek at early December auction market summaries:

-

East: Alabama hay prices were firm, with moderate supply and good demand. In Pennsylvania’s Lancaster area, large bales of alfalfa sold mostly $10 to $20 higher on good demand. Alfalfa/grass blended hay sold mostly steady on limited comparable receipts.

Large bales of grass hay sold mostly steady to $10 higher, while small bales remained steady. Straw prices were steady to $10 lower.

-

Southwest: All classes of California hay traded steady, with moderate demand. Recent rains had encouraged the emergence of winter grains and silage crops, and they were growing well. Silage corn grew well and harvesting was ongoing.

In Oklahoma, alfalfa trade and movement was mostly light to moderate. Demand was fairly good for all classes of alfalfa except grinding hay. Alfalfa prices were mostly $5 to $10 higher. Dairy hay offerings have become scarcer over the past few months.

Demand for better quality grass and wheat hay has also improved; however, movement remains light to moderate. In Texas, all hay classes traded steady on moderate to good movement after the Thanksgiving holiday.

-

Northwest: In Idaho, alfalfa sold steady. Most trading took place in the eastern part of the state. There was good demand for higher-testing alfalfa, with strong interest from California.

In Oregon, hay prices trended generally steady in a limited test. Retail/stable type hay remains in demand, but many producers have sold out for the year. In the Washington-Oregon Columbia Basin, Fair/Good alfalfa sold steady in a light test. Demand remains good for all grades of alfalfa, and demand for feeder hay has increased.

Coastal Bermuda producers in the east and south were done with their fourth cutting and now focused on delivering hay to customers. Utah hay prices were mostly firm, with trading slow on all qualities. Lower quality hay demand is light with good supplies.

In Montana, hay prices were fully steady, but activity was slow. Demand for alfalfa hay was mostly light to moderate, as warm conditions helped curb hay usage. Demand for grass hay and grass-alfalfa hay was moderate to good on steady prices compared with the last report.

Colorado prices were slightly higher, with activity light and demand good in all classes. Stored feed supplies were rated 1 percent very short, 3 percent short, 85 percent adequate and 11 percent surplus.

-

Midwest: In Iowa, hay prices were sharply higher with a firm undertone. In Missouri, hay movement remains slow, supplies are moderate, demand is light and prices are steady. Drought conditions in the southern part of the state continue to worsen.

Across Kansas, market activity is slow, with demand moderate to good and prices steady. Areas facing drought conditions are increasing. In Nebraska, alfalfa and grass hay sold fully steady to $5 higher; eastern dehydrated alfalfa pellets sold steady to $10 higher; Platte Valley pellets sold steady. Ground and delivered hay sold steady. Demand has improved as cattle moved into feedlots and producers need hay to supplement cows through the winter.

In South Dakota, prices remained steady to firm for all classes of hay. Demand for high-quality grass hay has improved as calves moved into feed yards. There is also demand for western lower quality alfalfa or grass hay suitable for beef cow rations.

In Wisconsin, there was some strength in the market across all classes of hay, with signs of continued strength going into winter. In southwest Minnesota, there’s an adequate supply of mixed hay at steady prices, but a limited supply of higher quality hay.

Drought area

USDA’s World Agricultural Outlook Board estimated 25 percent of U.S. hay-producing acreage was located in areas experiencing drought as of Nov. 28. In addition to ongoing dry conditions in Montana and western North Dakota and South Dakota, a large droughty swath now covers an area stretching from southern Iowa, southeastern Missouri, Oklahoma, Arkansas and Texas. Dry pockets are also in parts of the Southeast, Kansas, Utah and extreme southern California.

Check out the hay areas under drought conditions here: U.S. drought monitor

Fuel prices

The U.S. Energy Information Administration (EIA) estimated U.S. retail prices for regular gasoline averaged about $2.50 per gallon during the first week of December, down about 3 cents from the week before but 29 cents per gallon more than a year ago. U.S. on-highway diesel fuel prices averaged about $2.92 per gallon, unchanged from a week earlier but up about 44 cents per gallon compared with a year ago.

Dairy outlook: Margins expected to weaken

October 2017 U.S. milk production grew 1.4 percent compared with the same month a year earlier, picking up the pace after slowing somewhat in September.

Nationally, October milk cow numbers were down 1,000 head from September’s revised estimate, but still 65,000 head more than October 2016. Compared with a year earlier, the largest growth was in Texas (+25,000 head), Arizona and Colorado (each +9,000 head) and New Mexico (+8,000 head). California (-13,000 head) and Minnesota (-4,000 head) led decliners.

October 2017’s U.S. average milk price of $17.90 per hundredweight (cwt) was up just 10 cents from September, and up $1.30 compared with October 2016. The January-October 2017 average of $17.62 per cwt is $1.74 more than the same period a year earlier.

The slight improvement in milk prices was offset by higher soybean meal and hay prices, leaving the October income-over-feed-cost margin virtually unchanged from September, according to the USDA Farm Service Agency’s (FSA) MPP-Dairy calculations. Based on milk and feed futures prices as of Dec. 4, monthly margins are expected to decline through May 2018.

Beef outlook: Drought impacts culling

Cattle placements in large feedlots during October 2017 were 10 percent above October 2016, and feedlot inventories as of Nov. 1 were about 6 percent greater than a year earlier. An increase in overwinter forage availability and a larger calf crop will likely support strong placements into 2018.

The USDA raised beef production projections for 2018, forecasting heavier fed cattle weights. Fed cattle prices during the first quarter of 2018 are expected to be below year-earlier levels, reflecting increasing supplies of slaughter-ready cattle.

Cow slaughter well ahead of last year

The pace of 2017 beef and dairy cow culling remains well ahead of a year earlier. Through the first 10 months of 2017, beef and dairy cows slaughtered under federal inspection were estimated at 4.78 million head, about 325,000 more than January-October 2016.

With heavier slaughter rates, U.S. average cull cow prices declined.

October 2017 cull cow prices (beef and dairy combined) averaged $65.40 per cwt, down $4.50 from September and the lowest monthly average price since February 2017. Year-to-date, the cull cow price average is $70.93 per cwt, down $6.64 from January-October 2016. ![]()

-

Dave Natzke

- Editor

- Progressive Forage

- Email Dave Natzke