Based on the latest USDA Foreign Agricultural Service export estimates, U.S. alfalfa hay exports slumped in October, pressured lower by tariff-impacted sales to China. Total shipments of alfalfa hay fell to 197,718 metric tons (MT), the lowest monthly volume since January and February 2018. Year-to-date alfalfa hay exports are behind last year’s record-high pace.

October alfalfa exports to China totaled 40,761 MT, the lowest monthly total since January 2014. China, the leading U.S. alfalfa hay market since 2014, fell behind Japan. Sales to Saudi Arabia and the United Arab Emirates were also down from September.

October exports of other hay showed some improvement. At 115,140 MT, it was the highest monthly volume since March. Sales to Japan (62,241 MT) and South Korea (32,259 MT) were the highest since June, with Taiwan’s purchase of 11,696 MT the highest total of the year.

There is some news that could bring more cheer to hay exports. Meeting during the G20 Summit Meeting in Argentina on Nov. 30, President Donald Trump and Chinese President Xi Jinping declared a 90-day truce in an escalating trade war between the two countries, with the U.S. putting a hold on an increase in import tariffs scheduled for Jan. 1, 2019. Although there were reports coming out of the meeting that China pledged to buy more U.S. agricultural products, details were sketchy.

(Read "The U.S. is not the only dog in town: U.S. Forage Export Council update.")

October through February is normally the high season for U.S. exports, said Christy Mastin with Eckenberg Farms Inc. in Mattawa, Washington. But in addition to tariffs, strong typhoons that hit China, South Korea and Japan in early September and then again in early October caused shipping delays, reducing export totals.

Lest we forget the “present” spirit of the hay year, we’ll get a glimpse of hay stocks stored on farms as of Dec. 1, 2018, in USDA’s January Crop Production report.

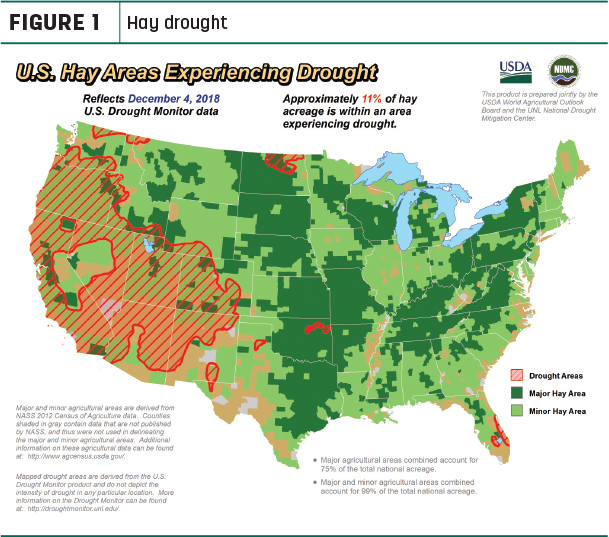

Drought areas

It’s also the time of year when Western water watchers dream about snowpacks and reservoirs.

The USDA World Agricultural Outlook Board’s latest drought maps changed little over the past month, with percentages of hay- and alfalfa-producing areas considered under drought conditions the lowest since late spring of 2017. Over the past month, drought areas of South Dakota, Montana and upstate New York dissipated, but dry conditions expanded in northern areas of Nevada and California.

Precipitation in the intermountain West improved current snowpack and long-term precipitation deficits, resulting in widespread improvements to long-term drought conditions in Utah, Colorado and northeast Arizona.

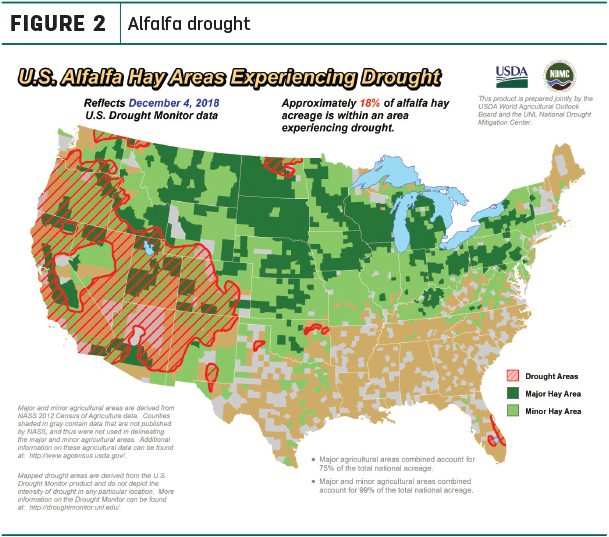

About 11 percent of U.S. hay-producing acreage was located in areas experiencing drought at the start of December (Figure 1), unchanged from early November. In alfalfa hay production areas, about 18 percent remained under drought conditions (Figure 2), also unchanged from a month ago.

Despite recent rains, California’s “water year” has started dry, and many of the state’s largest reservoirs are below average. The California Department of Water Resources announced an initial water allocation of 10 percent for the State Water Project contractors for the 2019 calendar year.

Hay prices mixed

The latest available USDA monthly Ag Prices report summarized October 2018 prices.

Alfalfa

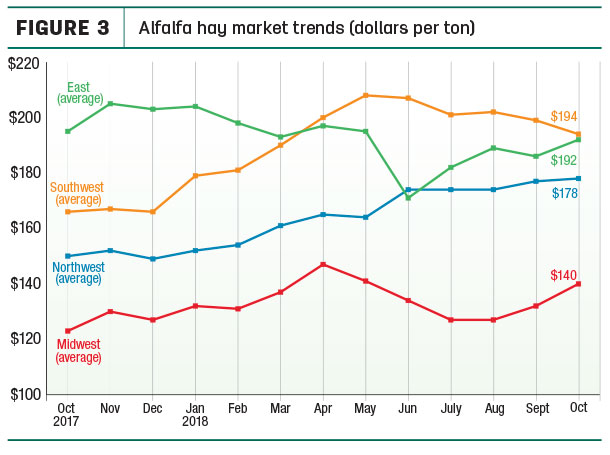

The national average alfalfa hay price was $178 per ton in October, down $2 from September, but still $25 per ton higher than October 2017. Regionally, prices rose in the East, Midwest and Northwest, but were lower in the Southwest (Figure 3).

Despite the lower overall national average, October average alfalfa hay prices rose $10 per ton or more in seven states compared to a month earlier, led by Iowa ($26) and Minnesota and Pennsylvania (both up $18 per ton). Those gains were offset by declines of $20 and $15 per ton in Arizona and Oklahoma, respectively.

Compared to a year earlier, alfalfa hay prices were up $50 or more per ton in Colorado, Oklahoma and New Mexico. New York reported a substantial price drop, down $44 per ton from October 2017.

High monthly alfalfa hay prices were in New Mexico ($230) and Kentucky and Colorado (both $215), and were at $200 or more in Oregon, Pennsylvania and California. The low price for the month, at $85 per ton, was in North Dakota.

Other hay

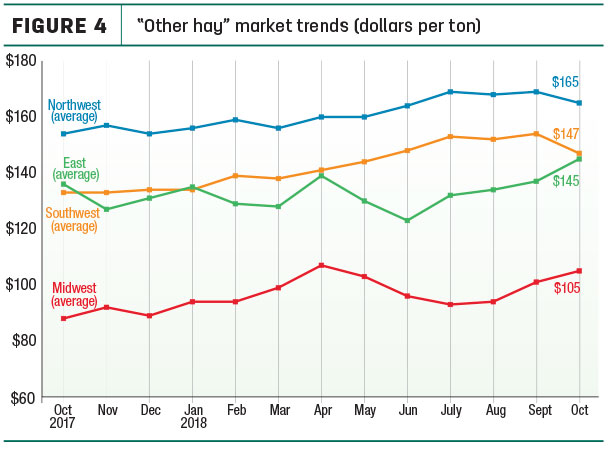

The U.S. average price for other hay was estimated at $132 per ton, up $2 per ton from September and $12 more than a year earlier.

Looking at regional breakouts, October 2018 average prices were higher in the East and Midwest, but lower in the Northwest and Southwest (Figure 4).

Among individual states, Minnesota and Pennsylvania saw the largest monthly increases, up $20 per ton. Price declines of $21 and $30 per ton were seen in Oklahoma and Idaho, respectively.

Highest average prices for other hay again hit $200 or more per ton in Colorado, Arizona and Oregon. North Dakota and Oklahoma saw monthly lows of $63 and $72 per ton, respectively.

(Read "Western hay prices – Where we’ve been and where we’re going.")

Organic hay

According to the USDA’s organic hay report, FOB farm gate prices at the end of November were:

- Supreme alfalfa large square bales – $250 per ton

- Premium alfalfa mid square bales – $200 per ton

- Good alfalfa mid square bales – $170 per ton

- Premium ryegrass small square bales – $215 per ton

No price reports were available for delivered organic hay.

Dairy margins better, temporarily

Lower hay prices and a slight improvement in the U.S. average milk prices helped improve dairy farmer income margins, at least temporarily.

At $8.96 per hundredweight (cwt), October 2018’s Margin Protection Program for Dairy (MPP-Dairy) income-over-feed-cost margin was the highest of the year. To put the year in perspective, however, 2018’s monthly average income margin is about $2.25 per cwt less than the same period in 2017. Current forecasts now put monthly margins between $8 and $8.50 per cwt from November 2018 through June 2019.

October 2018 U.S. milk production increased less than 1 percent from the same month a year earlier, as cow numbers dropped to their lowest level since February 2017. Eight states increased cow numbers compared to October 2017, led by Texas (+24,000 head), Colorado (+16,000 head) and Kansas (+9,000 head). In contrast, cow numbers in California and Ohio were each down 10,000 head, with Pennsylvania down 9,000 head. Cow numbers were also down a combined 16,000 head in Michigan, Minnesota and Wisconsin.

Regional markets

State conditions and market summaries as of early December follow:

• Midwest: In Kansas, alfalfa hay prices and sales remain steady, and producers are reporting they are receiving more inquiries. Winter weather has farmers feeding a little more hay.

In Missouri, wet, muddy conditions took over much of the state, and temperatures weren’t cold enough to keep the ground frozen. As a result, hay feeding has picked up, and grass stockpiles are diminishing. Many smaller producers and horse farmers are looking for hay.

Hay prices were steady in Nebraska, but many buyers were looking for cheaper sources of roughage to blend with their winter rations. Sellers with baled hay are hoping for an upward trend in the market, as supplies begin to run low and snowfall has hampered access to cornstalks still in the field.

Top-quality hay is in short supply in Iowa, and most are buying on an as-needed basis.

In South Dakota, prices for premium grades of hay were steady to higher, with good demand for all classes of hay and straw. Milk prices continue to impact the hay market. There is a demand for quality grass hay as cattlemen wean calves and move them to feedyards.

Most of the hay available in southwest Minnesota was in round bales, and are generally discounted.

In Wisconsin, there is demand for top-quality hay, just not much available. Low-quality hay is discounted depending if it was stored or was on the fencerow.

• Northwest: In Wyoming, hay demand was moderate across most reporting regions. Some cattlemen were on the fence trying to decide on whether to procure additional hay inventory or sell off some older cows.

In Montana, alfalfa hay sold fully steady on heavy offerings. Sales to out-of-state markets were good, with western and southern neighboring states adding to demand.

In Idaho, all grades of alfalfa sold steady to firm. Demand for feeder and organic alfalfa exceeds supply.

In Oregon, retail/stable-type hay remained most in demand; prices trended steady to higher. In the Columbia Basin, there’s more interest shown by exporters and feeder hay buyers. Exporters are buying fully wrapped hay.

• Southwest: In Oklahoma, alfalfa trade was mostly slow, but threats of a major winter storm over the second weekend of December had supported some last-minute hay buying. Demand for good quality grass hay has increased, with supplies and offerings limited; there is a great deal of low-quality grass hay on hand.

In the Texas Panhandle, livestock owners were busy preparing for a winter storm and continued to buy or contract hay as it becomes available to stock up for the colder months ahead.

• East: In Pennsylvania, there weren’t enough sales of alfalfa to get an accurate market test. Large bales of grass and grass-alfalfa blended hays traded $10 to $20 higher, while small bales traded sharply higher. All varieties of hay sold firm at Lancaster; straw and fodder were sharply higher.

Other market factors

• Fuel prices: At $2.45 per gallon, the national average regular gasoline retail price started December 5 cents lower than a year earlier, but substantially higher prices were reported in the Rocky Mountain and West Coast regions. At $3.21 per gallon, the U.S. average diesel fuel price was up 29 cents from a year earlier. California diesel prices topped $3.90 per gallon.

• Farm economics: The number of U.S. farms restructuring debt by filing Chapter 12 bankruptcy in the past year was lower than a year earlier. However, filings were higher in regions most heavily dependent on dairy and row crops for income.

National analysis by American Farm Bureau Federation (AFBF) Chief Economist John Newton shows Chapter 12 filings totaled 468 for the fiscal year 2018 (Oct. 1, 2017-Sept. 30, 2018), down about 8 percent from a year earlier.

Regionally, Chapter 12 bankruptcy filings were higher than year-ago levels in district courts located in areas characterized by highly concentrated traditional row crop, livestock and dairy production.

• Interest rates: Meeting in early November, the Federal Reserve’s Open Market Committee voted to leave federal fund interest rates unchanged, and its chairman later hinted the Fed’s interest rate may be left unchanged when the committee meets again in mid-December. Nonetheless, third-quarter 2018 Federal Reserve Bank district reports showed interest on variable- and fixed-rate loans had moved to the highest levels since 2011-12. ![]()

-

Dave Natzke

- Editor

- Progressive Dairyman

- Email Dave Natzke